Utilizing GRATs after a Market Downturn

Over the past month, fear surrounding the continued spread of the coronavirus (COVID-19) and a global financial crisis, have caused deep dips in the stock market. On February 20, 2020, the S&P 500 opened at 3,380.45. A little over a month later, on March 23, 2020, the S&P 500 had dropped 33.8 percent, closing at 2,237.40. Although drastic drops in the stock market can cause investor panic, they also present unique estate planning opportunities for gifting assets with reduced values. A particularly useful gifting vehicle in this economic environment is a GRAT.

A Grantor Retained Annuity Trust (GRAT) is an irrevocable trust funded with a single contribution of assets, which pays back to the grantor a percentage of the initial contribution (the annuity) for a term of a minimum of two years and then distributes the assets remaining at the end of the term to beneficiaries other than the grantor.

The objective of a GRAT is to shift future appreciation on the assets contributed to the GRAT to others at a minimal gift tax cost. A GRAT can be, and is often, structured so that the present value of the annuity the grantor receives back from the trust is nearly equal to the value of the initial contribution. This results in a taxable gift of a negligible amount, and is often referred to as a "zeroed-out" GRAT. For the GRAT strategy to be successful, the assets transferred to the GRAT must appreciate at a rate greater than the IRS assumed rate of return. The difference between the actual rate of return on the investment and the IRS assumed rate of return will pass, gift tax free, to the beneficiaries (or most likely, to continuing trusts for their benefit) at the end of the GRAT. The current IRS assumed rate of return for April 2020 is 1.2 percent. This low assumed rate, coupled with increasing stock market volatility, makes GRATs an attractive option for taxpayers looking to shift wealth to beneficiaries free of any gift tax.

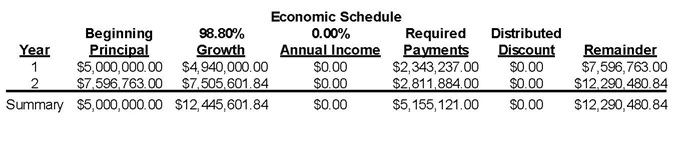

Funding a GRAT with stocks that have significantly dropped in value as a result of a market downturn can be a great way to increase the chances that the actual rate of return of an investment appreciates at a rate significantly greater than the IRS assumed rate of return. Taxpayers who utilized this strategy during the 2008 financial crisis were able to make significant tax-free gifts to beneficiaries through the use of zeroed-out GRATs. Below is an illustration of the economic schedule for a taxpayer who funded a zeroed-out two-year GRAT with $5 million worth of Apple stock in February 2009.

In the above illustration, the 98.8 percent annual growth represents the approximate annualized growth of Apple's stock from February 2009 through February 2011. Apple did not pay a dividend during this time period, so there was no annual income. The $12,290,480.84 remainder approximates the amount that would have passed to beneficiaries of the trust, free of any gift tax as a result of the hypothetical GRAT. Although Apple's stock performed remarkably well during this time period, it had fallen over 47 percent during the six-month period prior to February 2009, making a significant portion of its appreciation simply a recovery of its prior losses.

What if the stock placed in the GRAT were to recover its entire prior losses in the first year of the GRAT, and the investor wanted to lock in this gain from the GRAT? GRATs can be drafted to allow the grantor to reacquire property from the trust by substituting other property of equivalent value. At any time during the term of the GRAT, the investor could swap in cash (or other low-risk assets) in exchange for the stock initially transferred and effectively lock in the gain of the GRAT. Since a GRAT is typically considered a grantor trust for income tax purposes, there would be no income tax consequences from exchanging appreciated assets between the grantor and the grantor trust.

As stated above, for a GRAT to be effective as a wealth transfer tool, the assets must appreciate at a greater than the IRS assumed rate of return. If the assets in the GRAT lose value or appreciate at a rate less than the IRS assumed rate of return, then the beneficiaries will not receive any assets free of gift tax. Often this is referred to a failed GRAT. However, because a GRAT can be structured to be zeroed-out GRAT, a failed zeroed-out GRAT will simply leave the grantor in the same place, at least from a transfer tax standpoint, as they were upon funding the GRAT. For this reason, investors need not attempt to "time the market" to realize the benefits of GRAT planning; the current market volatility produces multiple opportunities to pass on significant wealth to the next generation.

DISCLAIMER: Information contained in this alert is for the general education and knowledge of our readers and is not intended to constitute legal, tax, accounting or investment advice. It is not designed to be, and should not be used as, the sole source of information when analyzing and resolving a legal problem. Moreover, the laws of each jurisdiction are different and are constantly changing. If you have specific questions regarding a particular fact situation, we urge you to contact your counsel at Holland & Knight LLP.